File:TED Spread Chart - Data 2008 zh-hant.svg

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

原始檔案 (SVG 檔案,表面大小:1,028 × 720 像素,檔案大小:169 KB)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

摘要

| 描述 |

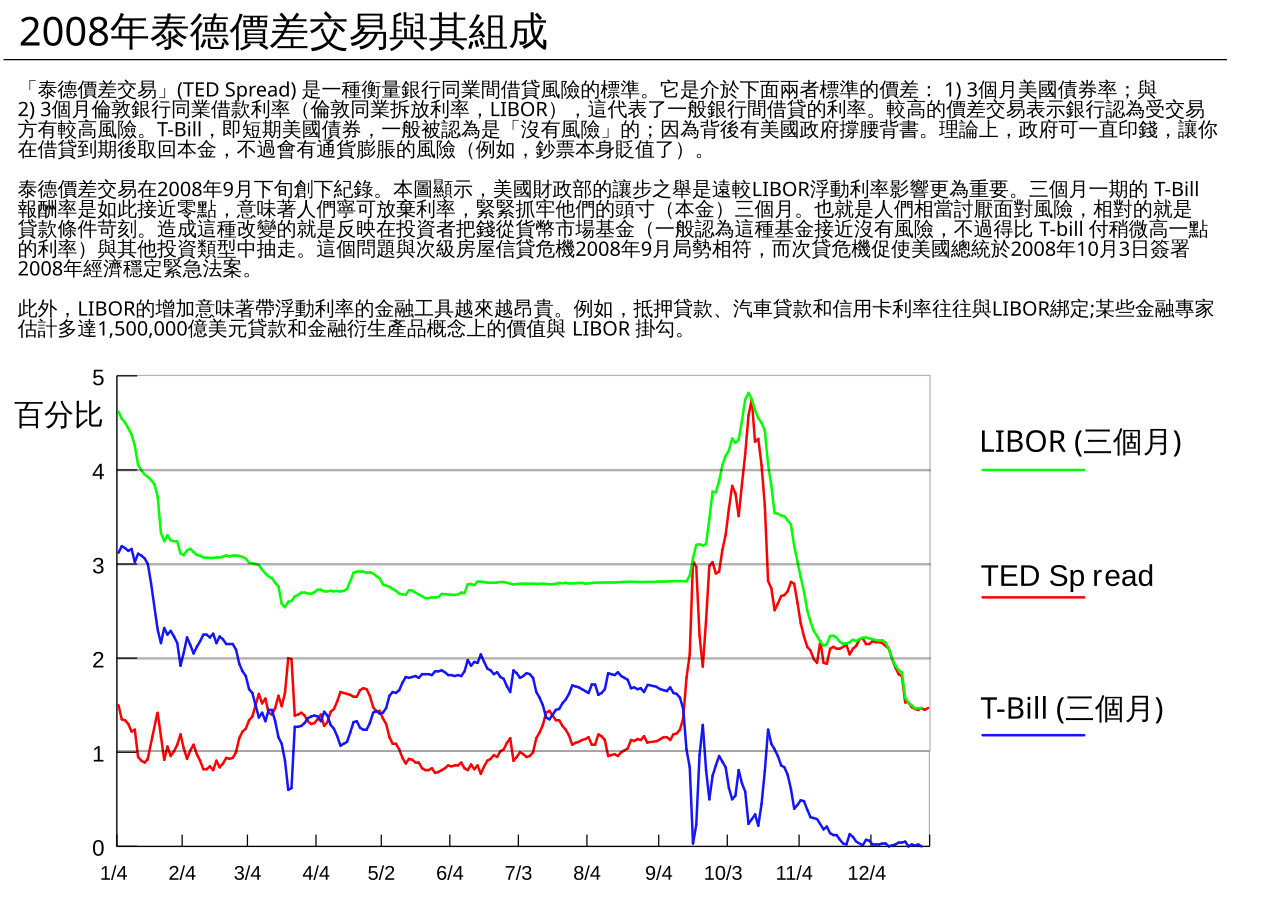

English: The “TED Spread” is a measure of credit risk for inter-bank lending. It is the difference between: 1) the three-month U.S. treasury bill rate; and 2) the three-month London Interbank Borrowing Rate (LIBOR), which represents the rate at which banks typically lend to each other. A higher spread indicates banks perceive each other as riskier counterparties. The t-bill is considered "risk-free" because the full faith and credit of the U.S. government is behind it; theoretically, the government could just print money so you will get your principal back at maturity, although there is risk of inflation (e.g., being paid back in cheaper dollars).

The TED Spread reached record levels in late September 2008. The diagram indicates that the Treasury yield movement was a more significant driver than the changes in LIBOR. A three month t-bill yield so close to zero means that people are willing to forego interest just to keep their money (principal) safe for three months--a very high level of risk aversion and indicative of tight lending conditions. Driving this change were investors shifting funds from money market funds (generally considered nearly risk free but paying a slightly higher rate of return than t-bills) and other investment types.[1] These issues are consistent with the September 2008 aspects of the subprime mortgage crisis which prompted the Emergency Economic Stabilization Act of 2008 signed into law by the U.S. President on October 3, 2008. In addition, an increase in LIBOR means that financial instruments with variable interest terms are increasingly expensive. For example, mortgages, car loans and credit card interest rates are often tied to LIBOR; some estimate as much as $150 trillion in loans and derivative notional value are tied to LIBOR.[2] |

| 日期 | Original date: October 4 2008; Upload date: January 19, 2009 |

| 來源 | en:File:TED Spread Chart - Data to 9 26 08.png |

| 作者 | Origin work by en:User:Farcaster; Chinese Translation by Zanhsieh |

| 其他版本 | en:File:TED Spread Chart - Data to 9 26 08.png |

{kind=link}

References

Sources

Three month treasury bill rates: St. Louis Federal Reserve Bank

Three month Libor rates: Bulgarian National Bank Tables

Another libor source: BBA

授權條款

- 您可以自由:

- 分享 – 複製、發佈和傳播本作品

- 重新修改 – 創作演繹作品

- 惟需遵照下列條件:

- 姓名標示 – 您必須指名出正確的製作者,和提供授權條款的連結,以及表示是否有對內容上做出變更。您可以用任何合理的方式來行動,但不得以任何方式表明授權條款是對您許可或是由您所使用。

- 相同方式分享 – 如果您利用本素材進行再混合、轉換或創作,您必須基於如同原先的相同或兼容的條款,來分布您的貢獻成品。

檔案歷史

點選日期/時間以檢視該時間的檔案版本。

| 日期/時間 | 縮圖 | 尺寸 | 使用者 | 備註 | |

|---|---|---|---|---|---|

| 目前 | 2009年1月27日 (二) 23:33 | | 1,028 × 720(169 KB) | Zanhsieh | {{Information |Description={{en|1=The “TED Spread” is a measure of credit risk for inter-bank lending. It is the difference between: 1) the three-month U.S. treasury bill rate; and 2) the three-month London Interbank Borrowing Rate (LIBOR), which repr |

| 2009年1月20日 (二) 05:41 |  | 1,028 × 720(163 KB) | Zanhsieh | {{Information |Description={{en|1=The “TED Spread” is a measure of credit risk for inter-bank lending. It is the difference between: 1) the three-month U.S. treasury bill rate; and 2) the three-month London Interbank Borrowing Rate (LIBOR), which repr |

檔案用途

下列頁面有用到此檔案:

{kind=link}